What Is a Loan Decisioning Engine? How It Works and Features

When it comes to lending, nobody wants to lose a potential customer just because the approval process took three days longer than it should have. Even if that may be so, speed is not the only goal. Sometimes, a rushed underwriting process can quietly turn into a default problem six months later. This is exactly where a loan decision engine balances the equation. Not by introducing fluffy features but by actually operationalizing the stalled underwriting process. For decades, manual reviews, compliance pressure, and scaling issues have kept real lending at bay. The software allows lenders to automate credit evaluations, reduce manual bottlenecks, and make real-time lending decisions using data, rules, and risk intelligence.

In this article, lenders will gain a thorough understanding of what a loan decision engine is, how it works, and the key features to look for when implementing it.

What is a Loan Decisioning Engine?

The loan decisioning engine software is a rule-based system built not only to evaluate borrower applications but also to assess the risk associated with those applications. After verifying the prospect data, the system automatically produces underwriting decisions, distinguishing high-intent leads from low-intent ones.

Part of the reason loan decisioning engines are being hyped is that lenders are no longer operating in an era where manual reviews were still considered operationally acceptable. Time has become the real parameter to judge. The faster you respond to applications, the better. And that is only possible if automation takes the lead.

How Does the Loan Decisioning Engine Work?

If the current lending dynamic is anything to go by, borrowers are no longer sitting around refreshing their inboxes for three days. If the experience feels slow or disconnected, they move on. Instantly.

Borrower Data Enters the System

The process begins when a lead submits an application via a mobile app or an embedded finance interface. Unlike traditional underwriting workflows, the system does not wait to review applications manually, one by one. Instead, the loan decisioning engine pulls borrower data from multiple sources through integrated APIs and organizes it accordingly. The key details include income details, repayment history, requested loan amounts, and employment history. Since the engine is not based on static credit scores, the overall evaluation is transparent, with the minimum possible default risk. With such consistent decision-making in place, the system also creates that consistency later in the process.

Risk Rules and Models: Evaluate the Applicant

Speed is valuable, sure. But approving the wrong borrower faster cannot be a winning strategy. Especially when money is at stake. And that is where lending policies, credit models, and decision logic start working together in real time. After assembling the borrower profile, the loan decisioning engine evaluates the applicant based on predefined approval criteria. For instance, the engine automatically assesses the following:

Debt-To-Income Ratios

Credit Utilization Levels

Repayment History

Minimum Income Thresholds

Employment Stability

Existing Liabilities

Transparent risk evaluation matters because no two borrowers have the same profile, employment history, or credit score. And even if they have the same credit score on paper, underneath, financial behaviors differ. A perfectly designed loan decisioning engine captures those nuances consistently throughout the process.

Compliance and Verification Checks Run Automatically

Given the increasing regulatory pressure on lending firms and institutions, risk evaluation alone is insufficient to approve a loan safely. Whether it's fraud scrutiny or regulatory pressure, the current lending sphere is under tighter compliance checks. This means lenders have to scale while staying compliant throughout the underwriting process.

A well-developed loan decisioning engine automatically runs compliance and verification checks. And lenders need such technology more than ever. Not to replace underwriting altogether, but to ensure compliance. Because once the application moves forward, the engine instantly runs those verification checks. These may include:

KYC (Know Your Customer) Verification

AML (Anti-Money Laundering) Screening

Document Authentication

Sanctions And Watchlist Checks

Address And Identity Matching

Fraud Detection Triggers

Income And Employment Verification

If the engine spots any anomaly in these checks, it flags the lead instantly.

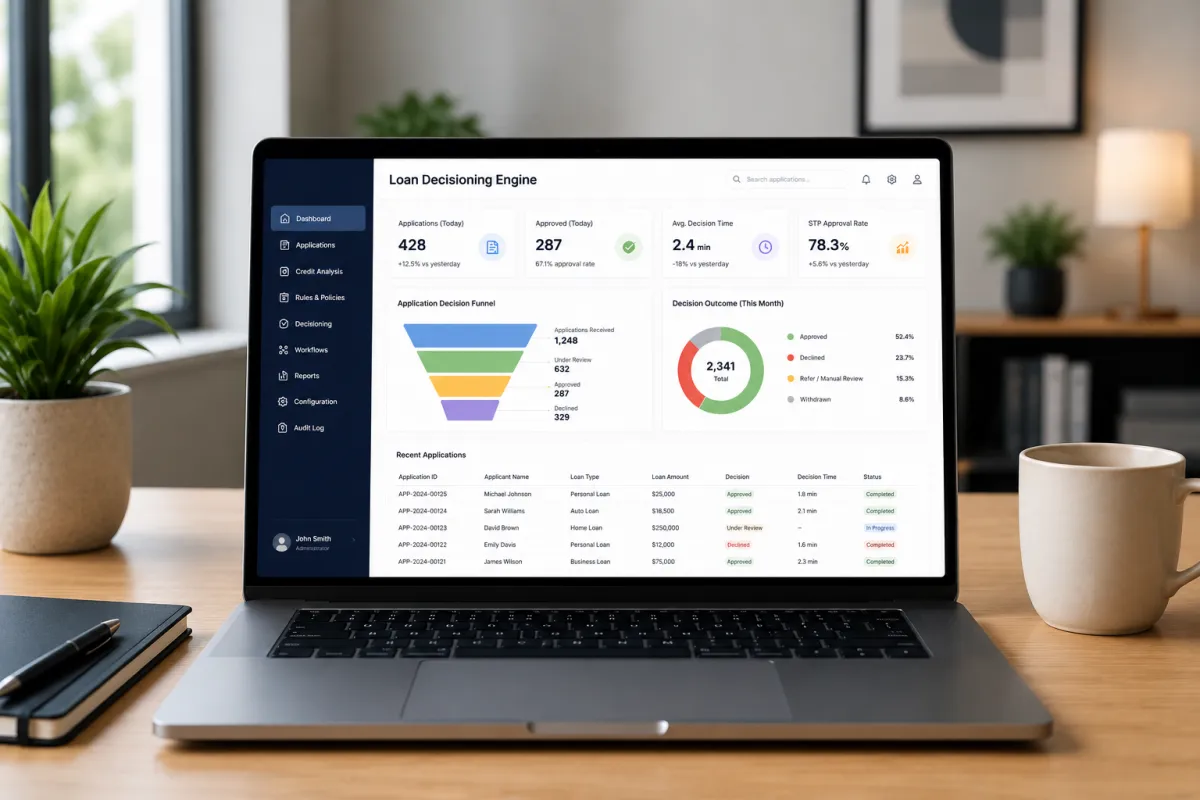

The System Produces a Lending Decision

Once risk analysis and compliance checks are done, the loan decisioning engine generates the final outcome. Based on predefined policies and rules, the engine either approves, rejects, or routes the lead to a manual underwriter for further review. Underneath all this process lurks the most fundamental goal: to apply lending policies uniformly, regardless of application volume or channel. When portfolios start scaling rapidly, having such a system in place becomes an imperative.

5 Key Features of a Loan Decisioning Engine Software

Real-Time Decisioning

Unlike legacy methods for evaluating leads, modern loan decision engines give lenders an edge over their competitors, not by applying grey-hat tactics but by actually streamlining decision-making. From the point a lead enters the funnel to loan approval, the system runs multiple eligibility and compliance checks. Be it KYC/AML checks or employment history analysis, the software does all the work in milliseconds. The immediate impact of having such a system in place is that teams can focus on matters that need more attention. But real-time decisioning is less about speed and more about making accurate decisions without compromising risk controls or compliance standards.

For lenders, this creates measurable operational advantages:

Shorter Underwriting Cycles

Reduced Manual Review Dependency

Faster Borrower Onboarding

Improved Application Completion Rates

More Efficient Handling Of High Loan Volumes

Configurable Decision Rules

Every organization or startup has its own predefined rules, eligibility criteria, and credit policies. This means that no two lending portfolios operate the same way. For example, a fintech startup focused on scale and a legacy system handling SME financing will evaluate risk very differently. Since this is the case, the loan decisioning engine allows lenders to create and adjust decision rules in line with their own policies.

For example, lenders can define the following:

Minimum Credit Score Thresholds

Income Verification Requirements

Debt-To-Income Ratio Limits

Geographic Restrictions

Loan Amount Conditions

Fraud Risk Triggers

This flexibility becomes especially important when portfolios begin to scale or new lending products enter the market.

Fraud Detection and Identity Verification

As loan approvals are getting faster, fraud has also become more sophisticated. While lenders today are evaluating borrower eligibility, they are also constantly filtering out synthetic identities, account takeovers, and suspicious application behavior. And, in this regard, manual decision-making is more prone to error. The automated loan decisioning engine validates borrower information across multiple data sources. At the same time, fraud detection models analyze behavioral and transactional signals that may indicate risk underneath the application.

For example, the engine can flag the following:

Mismatched Identity Records

Unusual Device Or Location Activity

Duplicate Applications

Manipulated Bank Statements

Suspicious Transaction Behavior

Synthetic Identity Indicators

Not only does this proactive approach help lenders detect fraudulent practices, but it also allows them to keep scaling at uncompromised speed and agility.

Compliance and Audit Readiness

Regulators increasingly expect lenders to demonstrate how decisions are made, which policies were applied, and whether compliance standards were consistently followed throughout the entire workflow. If processes somehow lag regulatory alignment, penalties become a foregone conclusion. A loan decisioning engine helps create that structure automatically. All verification checks, policy rules, risk evaluations, and approval actions are logged within the system, creating a clear audit trail for internal reviews and regulatory reporting.

Seamless Integration

Modern lending relies on multiple systems. It cannot operate in isolation. From loan origination platforms and banking APIs to fraud detection tools, CRMs, and payment gateways, modern loan decisioning engines integrate these systems. So instead of switching between disconnected systems, lenders can centralize underwriting operations within a single infrastructure.

A modern integration-ready decisioning engine can support the following:

Credit Bureau And Open Banking Integrations

KYC and AML Verification Providers

Loan Origination Systems (LOS)

Crm And Customer Onboarding Platforms

Payment Processing Systems

Conclusion

Decisions work best when they are consistent enough. Because today’s lending landscape is more about agility and less about approving more and more applications. And if current underwriting dynamics are anything to go by, manual intervention cannot really maintain the balance that is needed right now. The loan decisioning engine, however, with its automated nature, built-in compliance-check protocols, and fraud-detection capabilities, is the best fit for lenders trying to outperform their competitors. And honestly, that shift is already happening across the lending industry. Borrowers expect seamless experiences. Competition is moving faster. Risk environments are becoming more dynamic. Manual processes simply struggle to keep up at scale.